The Reserve Bank of India (RBI) “remains in readiness to operationalize central bank digital currency (CBDC) as and when necessary… with the eventual decline in the usage of (physical) currency gaining traction.” According to the RBI report, CBDC has the potential to bring about a sea change in payment transactions and quicken transmission, but poses a risk of disintermediation of the banking system, although this risk can be mitigated with a two-tier remuneration system for CBDCs, whereby transaction balances held by an individual remain interest free and are subject to a ceiling while CBDC balances of the individual over and above the ceiling are subject to a penal negative interest rate.

LSE Economist Jon Danielsson argues that most of us would not want to live in a society where bitcoin succeeds, although the internal contradictions and perverse consequences of crypto-asset success mean that they are destined for failure. The value proposition for bitcoin is that it will displace fiat money, and Danielsson argues that there can only be either full displacement or no displacement, but full displacement is not desirable or feasible. If it succeeds (full displacement) the big holders (“whales”) will become the wealthiest people in the world, and this would lead to greater inequality, social division and populism. However, if bitcoin becomes that successful, national authorities will jump in to protect their fiat currency monopolies, at which point the value of bitcoin heads to zero.

According to the latest report from Glassnode, institutions and investors holding a large amount of Bitcoin reduced their holdings by 140,000 Bitcoins in February.

* The views expressed herein are those of the author and should not be attributed to the International Monetary Fund, its Executive Board or its management.

The U.S. Securities and Exchange Commission (SEC) published the framework in which the agency will examine digital asset investments. Demanding regulatory compliance across areas ranging from custody, bookkeeping, registration requirements to conflicts of interest protocols, the SEC has made it clear to major broker-dealers and investment advisers that digital assets will face similar levels of scrutiny as traditional securities.

Flare Networks will integrate Stellar Lumens (XLM) with its smart contract platform, thereby offering compatibility with the Ethereum blockchain. Users will be able to create XLM-backed tokens and use those tokens with Ethereum-based DeFi projects. While Stellar already supports native smart contracts, its own contracts are not compatible with the Ethereum Virtual Machine. Flare Networks has previously announced integration with XRP, Litecoin, and Dogecoin.

* The views expressed herein are those of the author and should not be attributed to the International Monetary Fund, its Executive Board or its management.

I’ll be publishing my next monthly Fintech Monitor on Monday, but here’s an update on last edition’s discussion of algorithmic stablecoins – both bad news and good news!

This U.S. Federal Reserve paper identifies some high-level environmental preconditions that support a general-purpose CBDC in the United States. These preconditions are necessary, though not sufficient, and can be broadly grouped into five areas: clear policy objectives, broad stakeholder support, strong legal framework, robust technology, and market readiness. Within each area, detailed elements are discussed. These areas and elements are not exhaustive because many systems, tools, processes, and structures will need to be in place for a CBDC. In addition, many of these elements are interconnected. For example, engaging with a broad array of stakeholders and monitoring market readiness could inform clear policy objectives and vice versa. The paper does not attempt to prescribe how to address these preconditions; it aims to spark further inquiry.

The Bank of Jamaica (BOJ) announced plans to begin a central bank digital currency (CBDC) pilot in the second or third quarter of 2021. Over the last couple months, the BOJ has undertaken the requisite preliminary work relating to assessments and protocols aimed at receiving government approval for a pilot to run for a couple of months and be finished by the end of the year. If the pilot is successful, the BOJ aims to issue the new CBDC to the public in early 2022. The BOJ highlighted the benefits of CBDC which include increased financial inclusion, and providing another means of efficient and secured payments. Also, for deposit-taking institutions, the BOJ claimed that CBDC represents an opportunity to improve cash management processes and costs.

As the law will determine what type of central bank digital currency (CBDC) can be issued in each jurisdiction, getting the legal model right is a crucial step in introducing one. The current statutory language seems to provide the ECB with enough room to offer a digital euro directly to the public through digital accounts if it so chooses. However, for example, the US and Brazilian central banks are authorized to establish relations only with a limited set of institutions, notably banks, not with people or corporations. Without a change to these rules, digital dollars and digital reais would have to be distributed to the public through intermediaries, just like cash is made available today through banks. For all central banks considering issuing a CBDC, the time to tackle the legal troubles and seek legislative reform is now, because reaching a political consensus on this model may take time, since CBDCs raise many contentious issues, from changing the business of banking to creating new privacy risks.

The Bangko Sentral ng Pilipinas (BSP) established the Payments and Currency Management Sector (PCMS) to manage the interplay of physical currency and digital money. PCMS is tasked to maintain the safety and integrity of the local currency and to ensure a well-functioning payments and cash ecosystem that supports sustained and inclusive economic growth, in alignment with the BSP’s Digital Payments Transformation Roadmap. The new sector, which consolidates existing currency and payment management units, is responsible for producing banknotes, coins, and securities documents; refining gold; and printing of cards for the national ID.

The Bank of Ghana has launched a new regulatory and innovation sandbox to provide a controlled testing environment for new financial products and services, in partnership with US-based technology firm Emtech. Emtech has built cloud-based software specifically for central banks. It said the sandbox would allow financial firms to interact with the central bank to test digital financial products while evolving [an] enabling regulatory environment. The sandbox is open to banks, specialised deposit-taking institutions and payment service providers.

“Bitcoin is vulnerable to government surveillance and prohibitions that could quash crypto exchanges and drive trades underground. But it arguably could survive underground better than could a banking system based on commodity redeemability that must be openly accessible to be trustworthy. If Bitcoin will continue to thrive as an investment and medium-of-exchange-in-waiting “until the authorities do better” at managing fiat money (and at allowing financial privacy), then Bitcoin may thrive for a long time to come.”

* The views expressed herein are those of the author and should not be attributed to the International Monetary Fund, its Executive Board or its management.

The last Monthly Monitor talked about how USD-pegged Empty Set Dollar (ESD) briefly held the #6 position in the stablecoin league table. The ESD launched in September 2020 and was one of the first algorithmic stablecoins to come to market. (An algorithmic stablecoin adjusts its supply to maintain its peg.) However, ESD broke its peg massively in January 2021, and is now trading down around $0.13 resulting in a drop down to #14.

However, there’s another very viable-looking USD-pegged stablecoin, TerraUSD which sits at #7 ($590 million market capitalization). The peg isn’t absolutely perfect, as it has occasionally spiked down to nearly $0.96 and up to $1.04, but since it has launched in October 2019 it has spent most of its time within a $0.98 – $1.02 band, which is better than any other algorithmic USD-pegged stablecoin I’ve seen. TerraUSD is also part of the Terra family of products that seem to be seeing real use cases (see below).

Terra is a delegated proof of stake system that uses the LUNA token as collateral for the stablecoins it issues, and it has several active use cases underway:

The South Korean CHAI decentralized app-based mobile payments system runs on Terra’s payment rail. The rail is built on two the native stablecoin of Terra for funds across the networks and the Luna token for small transaction fees for miners. CHAI has partnered with 15+ major local banks to facilitate convenient fiat on/off ramps, recently crossed 2 million monthly active users. Terra’s network also integrates with MemePay, a Mongolian e-wallet utilized by 1.5% of the online population.

Terra’s Mirror synthetic assets protocol tracks the price of U.S. stocks, futures, exchange-traded funds, and other traditional assets. The Mirror Wallet kicked off with 12 of the top American technology stocks. The target market is users outside of the United States who seek 24/7 exposure to and fractional ownership of synthetic assets.

FYI besides TerraUSD there are eleven other Terra-based stablecoins (AUD, CAD, CHF, CNY, EUR, GBP, INR, JPY, HKD, KRW, and SGD).

Coinbase has publicly filed an S-1 with the U.S. Securities and Exchange Commission (SEC) outlining its plans to complete an initial public offering (IPO) on the NASDAQ. Accrording to the filing, Coinbase intends to raise up to $1 billion and trade under the ticker symbol of “COIN.”

Canadian digital bank VersaBank plans to launch a Canadian dollar-pegged stablecoin. VCAD will be issued by VersaBank to financial intermediary partners in exchange for Canadian dollar deposits. The partners will then offer VCAD directly to individuals and businesses for use in commerce. VCAD will be redeemable for Canadian dollars as required.

With a few days left in February, decentralised exchange (DEX) processing volumes furing the month have surpassed $60 billion, according to Dune Analytics, already higher than January’s record level.

The Mauritius Financial Services Commission (“FSC”) issued a consultation paper proposing the setting up of a comprehensive regulatory framework for a FinTech Service Provider Licence which will aim at offering providers of technology services to financial institutions with a set of guidelines to be adhered to, should they wish to operate in or from Mauritius.

* The views expressed herein are those of the author and should not be attributed to the International Monetary Fund, its Executive Board or its management.

Yesterday I reported that Bitfinex and Tether reached a $18.5 million settlement with the New York Attorney General (NYAG) over allegations that they hid the loss of commingled client and corporate funds and misrepresented the truth about the reserves backing Tether’s USDT stablecoin. However, the lawsuit did not cover the rumored role of Tether in a huge BTC pumping scheme. I discuss some of these broader issues in a new blog post here.

On February 13, 2021, Bitt, in partnership with the Eastern Caribbean Central Bank (ECCB), executed the first successful retail central bank digital currency (CBDC) consumer-to-merchant transaction using DCash, the ECCB digital currency. The transaction was completed at Geo F. Huggins’ Foodland, in the island of Grenada. The ECCB has begun to issue DCash to participating financial institutions to enable customer purchases at selected merchants, as part of the closed segment of the DCash pilot. This live exercise is the final step before the public launch in four of the ECCU’s eight sovereign member countries (Antigua and Barbuda, Grenada, Saint Kitts and Nevis and Saint Lucia).

Ant-backed MYbank and Tencent-backed WeBank will reportedly join the Peoples’s Bank of China (PBOC) digital yuan pilot. The e-wallets from the two firms will have exactly the same functions as those from the six state-owned lenders in the trial.

The U.S. Securities and Exchange Commission (SEC) filed an amended complaint towards Ripple, accusing the firm of purposely misleading investors in relation to its XRP crypto-asset. The original complaint accuses Ripple Labs and its lead executives of being in violation of securities laws with $1.3 billion generated from XRP sales. It now alleges that they purposely manipulated XRP’s price by increasing and decreasing XRP sales depending on market conditions.

Square purchased $170 million Bitcoin, raising its holdings to about 5% of the company’s cash and equivalents. Square reported that crypto-assets continue to be a growing part of its business through the use of its Cash App for Bitcoin transactions. The financial payments company’s involvement with Bitcoin is a reflection of CEO Jack Dorsey’s belief in crypto-assets and the open internet.

According to crypto market data aggregator, Glassnode, Bitcoin whales offloaded massive amounts of BTC during February. The whales (who hold between 1,000 and 10,000 BTC) and humpback (more than 10,000 BTC) buying spree peaked in January as they snapped up 80,000 BTC, but so far in February they appear to have taken heavy profits, offloading 140,000 BTC.

Since its first cohort in 2016, the U.K. Financial Conduct Authority (FCA) Regulatory Sandbox has supported 14 digital ID models. Also, there have been 15 applications for Direct Support to the FCA Innovation Hub and 6 of these are now receiving that support. Many other digital ID providers have engaged with the FCA through various channels such as the Anti-Money Laundering TechSprints. The FCA, in collaboration with The City of London, has also recently completed a pilot Digital Sandbox, which provides data access and a digital testing environment to help innovative businesses develop proof of concept. Two digital ID propositions participated in the pilot.

* The views expressed herein are those of the author and should not be attributed to the International Monetary Fund, its Executive Board or its management.

Bitfinex and Tether reached a $18.5 million settlement with the New York Attorney General (NYAG) over allegations that they hid the loss of commingled client and corporate funds and misrepresented the truth about the reserves backing Tether’s USDT stablecoin. The two firms also agreed to provide to the NYAG quarterly reports on the composition of Tether reserves over the next two years, starting within ninety days of the February 18, 2021 effective date of the settlement. Without admitting or denying any wrongdoing, Tether committed to publicly share these reports. However, the lawsuit did not cover the rumored role of Tether in a huge BTC pumping scheme.

According to the Financial Stability Board, stablecoins are crypto-assets that aim to maintain a stable value relative to a specified asset, or a pool or basket of assets. U.S. dollar pegged USDT is the biggest stablecoin by market capitalization.

Although USDT’s market capitalization is a small fraction of BTC’s ($35 billion versus $940 billion on February 24, 2020) in terms of trading volume it is by far number one. USDT’s main use case appears to be as a crypto-asset trading on-ramp for residents of countries where there are crypto-asset trading bans and/or capital controls, and as a “reserve currency” for unbanked exchanges.

Is USDT fully backed U.S. dollar assets?

Tether claims that USDT is always 100% backed by currency and cash equivalents, plus “other assets and receivables from loans made by Tether to third parties, which may include affiliated entities.” In an ongoing lawsuit launched in 2019 by the New York Attorney General (NYAG) against Tether parent iFinex, it came to light that Tether had loaned $850 million of USDT’s reserves to its sister company Bitfinex. Since then, Tether has been dogged by suspicions that USTD is not 100% backed by U.S. dollar assets, although Tether claims that the Bitfinex loan has been paid off.

Tether has not helped its cause with its opacity regarding USDT’s reserve holdings. Although not audited, other stablecoin issuers at least publish monthly attestations that they are fully backed. However, attestations remain very vague about what comprises the reserves. The last time Tether published anything like an attestation for USDT was in 2017., but claim full details will be released later in 2021.

What kinds of assets back USDT?

But even if USDT’s are fully backed, questions remain around what they are invested in, although the other stablecoin issuers are not paragons of transparency. The USDC attestation report only tells us the reserves are held in segregated accounts at US federally insured depository institutions and in approved investments. The BUSD and PAX reports are equally vague, telling us that the reserves are held at US depository institutions sometimes in amounts backed by debt instruments expressly guaranteed by the full faith and credit of the US Government. Gemini’s attestations seem more transparent and imply that all of the reserves are invested in US Treasury securities.

The perception that Tether’s investments aren’t exactly top-tier, is not contradicted by the redemption restrictions: “Tether reserves the right to delay the redemption or withdrawal of Tether Tokens if such delay is necessitated by the illiquidity or unavailability or loss of any Reserves held by Tether to back the Tether Tokens, and Tether reserves the right to redeem Tether Tokens by in-kind redemptions of securities and other assets held in the Reserves.” (Crypto traders get around this by buying BTC with USDTs on an exchange that trades the BTC/USDT pair, transferring them to an exchange that trades the BTC/USD pair, and cashing them out.)

Is Tether part of a Bitcoin pumping scheme?

Some claim that USDT issuance is part of a BTC price pumping scheme. For example, a 2019 paper found that Bitcoin purchases with Tether “are timed following market downturns and result in sizable increases in Bitcoin prices. Rather than demand from cash investors, these patterns are most consistent with the supply-based hypothesis of unbacked digital money inflating cryptocurrency prices.” See also David Gerard’s succinct description of the process in this Twitter thread.

But according to Frances Coppola, USDT’s asymmetric mechanics both support and disprove this claim. An opposing theory says that what look like BTC pumps are merely Tether reacting to BTC price volatility by supplying more “lubrication” to markets. The “lubrication” idea stems from Tether’s key role as a “reserve asset” for unbanked crypto platforms. Also, a recent paper used USDT deviations from its fiat currency peg to show that USDT acts as a “safe haven” for crypto-asset investors. They found evidence of significant premiums over parity during the crash in non-stable crypto-assets in early 2018 and during the March 2020 COVID-19 crisis. Discounts were found to derive from liquidity effects and collateral concerns. For example, USTD spiked to as low as around $0.90 in April 2017 when doubts were raging about the sufficiency of Tether’s reserves.

So, if BTC’s price is falling, investors wanting to cash out is likely to increase demand for USDT, which will in turn raise its price. In normal circumstances, arbitrage is probably sufficient to maintain the peg. But when BTC is experiencing high volatility – in either direction – demand for USDT can increase far faster than arbitrageurs can bring it down. To prevent the dollar peg breaking, therefore, Tether must respond to this extra demand by issuing more USDT. And issuing more USDT increases exchange liquidity, making it easier to purchase or sell BTC and therefore feeding the price movement. So wild swings in BTC’s price might not be triggered by USDT issuance, but they… can be fed by it.

Conclusions

If Bitfinex and Tether follow through on their commitment to be more transparent about Tether’s reserves, rumors about USDT being backed by flaky assets may be put to bed, although questions remain around possible Tether BTC pumping. Also, it is a big if! However, the NYAG settlement does reduce a major crypto market black swan risk if, as Bryce Weiner believes, the market plumbing absolutely depends on USDT, making it effectively too big to fail.

Bitfinex and Tether reached a $18.5 million settlement with the New York Attorney General (NYAG) over allegations that they hid the loss of commingled client and corporate funds and lied about Tether’s USDT reserves. Within ninety days of the agreement February 18, 2021 effective date, and on a quarterly basis thereafter for two years, the firms will be required to publish reports on the composition of Tether reserves. Without admitting or denying any wrongdoing, Tether committed to publicly share these reports.

A Swiss National Bank working paper proposes a token-based central bank digital currency (CBDC) system without distributed ledger technology. It shows how earlier-deployed, software-only electronic cash can be improved upon to preserve transaction privacy, meet regulatory requirements in a compelling way, and offer a level of quantum-resistant protection against systemic privacy risk. The CBDC proposed here is based on blind signatures and a two-tier architecture, that purportedly guarantees perfect, quantum-resistant transaction privacy while providing anti-money laundering and counter terrorism financing protections for society that are actually stronger than those of banknotes. Neither monetary policy nor financial stability would be materially affected because a CBDC with this design would replicate physical cash rather than bank deposits.

In a legal opinion on the European Union (EU) rules, the European Central Bank (ECB) said it should have the final word on whether a stablecoin should be allowed to launch in the euro zone. “Where an asset-reference arrangement is tantamount to a payment system or scheme, the assessment of the potential threat to the conduct of monetary policy, and to the smooth operation of payment systems, should fall within the exclusive competence of the ECB.” It added the proposed EU rules should be changed to say that its opinion on the matter is binding for national authorities assessing applications to issue stablecoins.

The Digital Currency Institute of the People’s Bank of China and the Central Bank of the United Arab Emirates have joined the m-CBDC Bridge central bank digital currency (CBDC) project for cross-border foreign currency payments. The m-CBDC Bridge initiative is run in partnership with the BIS Innovation Hub (BISIH), the Hong Kong Monetary Authority and the Bank of Thailand. It will further explore the capabilities of distributed ledger technologies by developing a proof-of-concept prototype to support real-time cross-border foreign exchange payment-versus-payment transactions in multiple jurisdictions, operating 24/7. It will analyse business use cases in a cross-border context with both domestic and foreign currencies.

Miners are frequently blamed for causing dips in the price of Bitcoin. These accusations are often unsubstantiated—worse still, they’re sometimes based on faulty metrics that conflate mining pool payouts with miner spending, ultimately misleading their users. This CoinMetrics research finds that, in line with the conventional wisdom, we find that miners tend to prefer Huobi and Binance to other exchanges, but flows from mining addresses represent a small percentage of total exchange inflows, about 5.5%, and are not a major source of market volatility.

This paper examines potential implications, complexities and risks associated with the proliferation of consumer-facing decentralized finance (DeFi) applications within financial services. It provides a taxonomical overview of DeFi applications and identify four key risks for managers, practitioners and scholars.

* The views expressed herein are those of the author and should not be attributed to the International Monetary Fund, its Executive Board or its management.

China’s Banking and Insurance Regulatory Commission (CBIRC) has tightened rules governing how online lending platforms fund their loans, a move that analysts say could hit the valuation of Jack Ma’s Ant Group. Under the rule changes online lending platforms will have to contribute 30 per cent of the funding for loans they offer in partnership with banks. The CBIRC will also cap how much capital commercial banks can commit to online lending in co-operation with tech platforms. The new rules will come into force next year.

The Securities and Exchange Board of India (SEBI) is reportedly cracking down on high-level executives who hold Bitcoin and intend to take their companies public in the coming months. SEBI has asked promoters of such companies to sell off any cryptocurrencies they hold before raising funds from the public, adding that investment bankers and securities lawyers involved with any ongoing Initial Public Offering (IPO) process were already informed of the new regulation.

Morocco’s central bank Bank-Al-Maghrib (BAM) has reportedly launched an exploratory committee to investigate the pros and cons of a central bank digital currency (CBDC) for the Moroccan economy. But this could be the same old news that was reported back in 2019 because there’s nothing new reported on the BAM website.

The only way to kill Bitcoin is to make it so that people don’t need it anymore. If no one wants a devaluation-proof, censorship-resistant, permissionless, borderless, non-discriminatory, teleporting financial asset, then no one will feed it energy, and it will die. Perhaps humanity can come up with another technology that addresses these needs. But until then, Bitcoin will thrive.

Non-Fungible Token (NFT) mania is now outpacing decentralized finance (DeFi). The search interest for NFT gained traction in the middle of January 2021, and last week more people were busy learning about digital collectibles more than DeFi in the US, as per Google Trends.

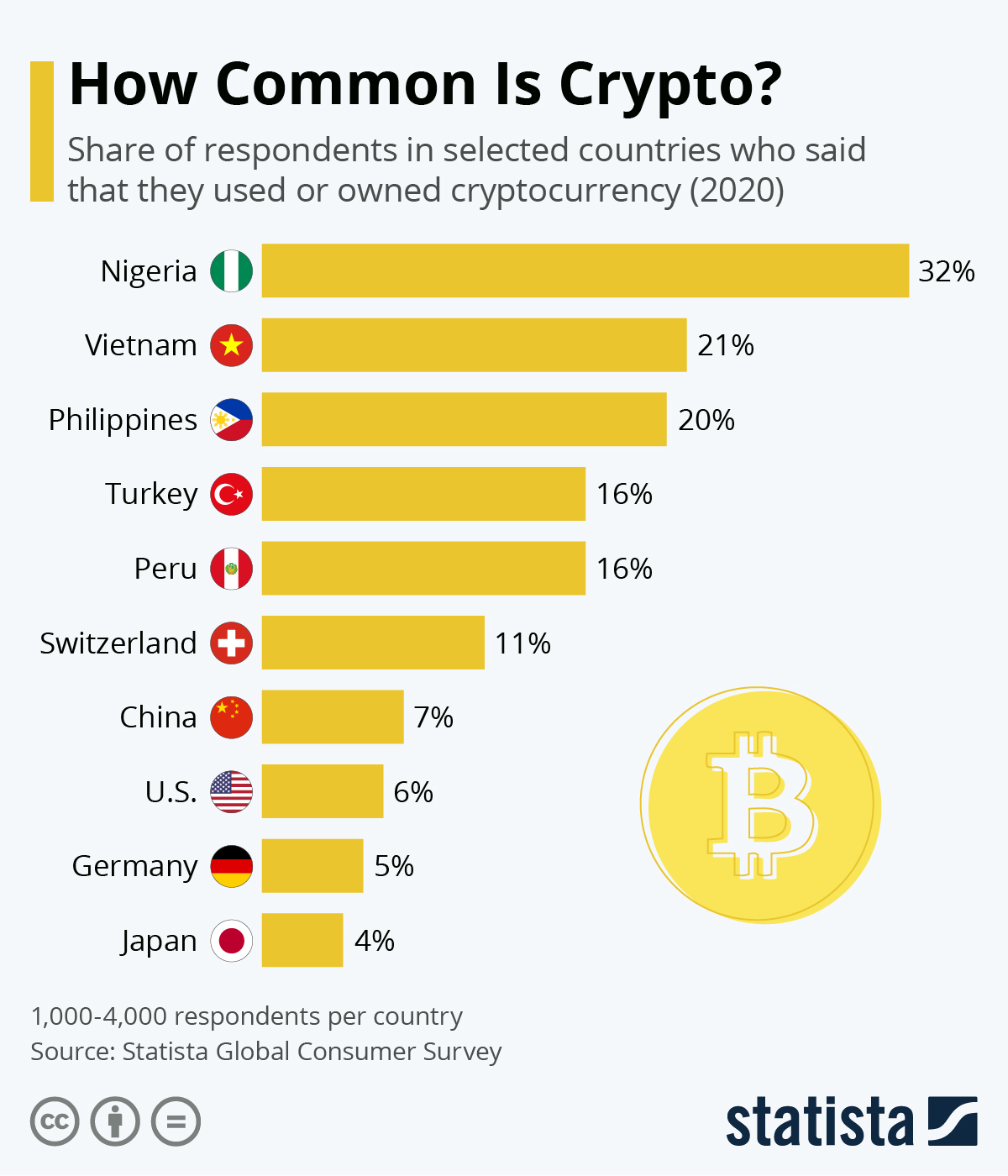

According to Statista, reliance on remittances and the prevalence of P2P phone payments have led to a steep rise of cryptocurrency use in Nigeria. Almost a third of Nigerians said this applied to them. Recently, businesses in the country have been adding crypto plugins to their phone payment options, adding another way in which Nigerians can use cryptocurrency in their everyday lives. The second and third highest rates of cryptocurrency use in the survey were recorded in Vietnam and the Philippines, respectively. Again, remittance payments play a role in the widespread use of cryptocurrency.

* The views expressed herein are those of the author and should not be attributed to the International Monetary Fund, its Executive Board or its management.